Bank sanctions December rate rise

The Bank of England (BoE) sanctioned a 15-basis-point increase in its main interest rate on 16 December and warned that inflation is now likely to hit 6% by spring.

At its latest meeting held in mid-December, the BoE’s nine-member Monetary Policy Committee voted by an 8-1 majority to raise Bank Rate to 0.25% from its previous historic low of 0.1%. This was the Bank’s first rate hike in more than three years and resulted in the BoE becoming the world’s first major central bank to raise rates since the onset of the pandemic.

The announcement was made a day after the Office for National Statistics (ONS) released the latest inflation data, which showed the cost of living is now rising at its fastest rate for 10 years. In the 12 months to November, the rate of inflation, as measured by the Consumer Price Index (CPI), surged to 5.1%. This was significantly higher than October’s 4.2% figure and above all forecasts in a Reuters poll of economists.

Speaking after announcing the rate hike, BoE Governor Andrew Bailey said that an outlook for “more persistent inflation pressures” had forced the Bank to act. Mr Bailey said, “We’re concerned about inflation in the medium term and we’re seeing things now that can threaten that. So that’s why we have to act.”

The Governor also revealed that the Bank now expects the CPI inflation rate to peak at around 6% in April, which would be three times above the BoE target figure. Although the rate is then expected to fall back across the second half of 2022, the Bank acknowledged that more “modest tightening of monetary policy” over the three-year forecast period “is likely to be necessary” in order to ensure inflation sustainably returns to its 2% target level.

UK growth rate stutters

Gross domestic product (GDP) figures released last month show the UK economic recovery had already lost momentum even before the emergence of the Omicron variant.

The latest GDP statistics show the economy expanded by just 0.1% in October, much weaker than the 0.4% consensus forecast predicted in a Reuters poll of economists. Growth was largely driven by a rise in face-to-face GP appointments at surgeries in England, although this was offset by a decline in industrial output, with production falling in both the electricity and gas, and mining and quarrying sectors.

In addition, a revision to previous GDP data revealed that the economy had actually grown at a slower pace during the third quarter. The new estimate puts July to September’s growth rate at 1.1%, rather than 1.3% as initially thought. As a result, the UK economy remains 1.5% smaller than its pre-pandemic level.

More recently, economic activity has been hit by the spread of the Omicron variant. Preliminary data from last month’s IHS Markit/CIPS Purchasing Managers’ Index (PMI) pointed to a sharp slowdown in UK private sector growth as rising virus cases hit consumer services spending.

The flash reading of the PMI’s composite output index fell to a 10-month low of 53.2 in December, leading CIPS Group Director Duncan Brock to describe the data as “grim news” for the UK economy. Mr Brook also said that positive gains over the last ten months had been “wiped out by yet another round of restrictions and curbs on consumers and businesses.”

Just before Christmas, the Chancellor unveiled a £1bn support package to help businesses hit by rising cases.

Markets (Data compiled by TOMD)

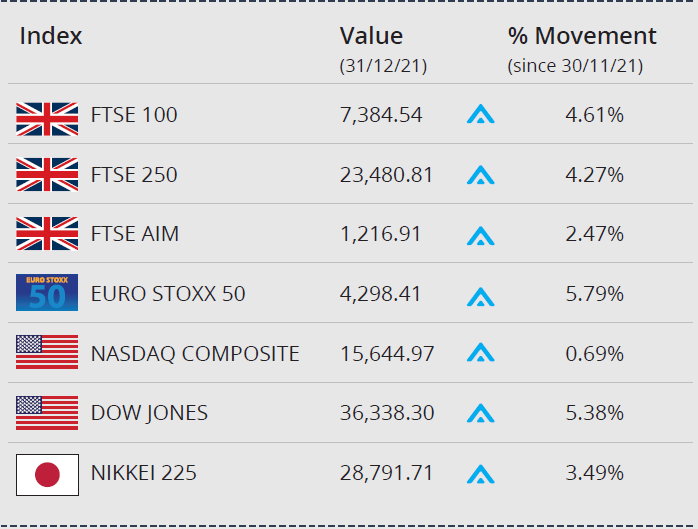

Major global indices closed December in positive territory. Despite escalating virus cases, stocks were supported by hopes that the Omicron variant is milder, potentially limiting fiscal impact as vaccines have allowed many economies to remain open.

In the UK, the FTSE 100 ended the year up 14.3%, registering its best annual gain for five years, as it continued to recover from its pandemic-induced lows of 2020. The FTSE 250, dominated by more domestically focused stocks, rose by 14.6%, while the AIM closed the year up just over 5%.

Wall Street led the way, with the Dow close to a record high at the end of December, rising over 5% in the month and by 18.72% in 2021, while the NASDAQ closed the year up over 21%. The US economy has proven resilient in the face of pandemic-related challenges. As with other global economies, inflation will be a focal point for investors going into 2022. Meanwhile, the Nikkei 225 ended the year on 28,791.71, up over 4.9%, its highest year-end level since 1989, and the Euro Stoxx 50 closed the year up just over 20% on 4,298.41.

On the foreign exchanges, sterling closed the year at $1.35 against the US dollar. The euro closed at €1.18 against sterling and at $1.13 against the US dollar.

Brent crude closed the year trading at around $78 a barrel, an annual gain of over 51%, its largest in 12 years. The price was lifted by higher demand as investors bet that surging virus cases would not derail the global economic recovery. Cautious production increases by OPEC+, the Organization of the Petroleum Exporting Countries plus allies, also helped to support the price. Gold is trading at around $1,805 a troy ounce, a loss of over 4.8% on the year. The price has been dampened by a stronger US dollar and the threat of a pullback in stimulus by major central banks, deterring many investors who favoured equities.

Labour market remains resilient

The latest set of employment statistics published by ONS suggests the UK labour market has withstood the end of the government’s furlough scheme and remains in a relatively robust state of health.

According to the most recent tax data, the number of people in payrolled employment continued to grow strongly, rising by a further 257,000 in November. This was the largest monthly increase since records began in 2014 and lifted the total number of workers on company payrolls to 29.4 million, 424,000 above pre-pandemic levels.

There was also positive news in terms of unemployment, with the headline rate in the three months to October falling to 4.2%; down from 4.3% in the previous three-month period. This suggests withdrawal of furlough at the end of September has not sparked a significant rise in redundancies. Although ONS did caution that some workers may still be working notice periods, it also said business survey responses suggest the number of redundancies was likely to be relatively small.

The data also showed job vacancies rising to another record high, with a total of 1.22 million jobs advertised in the three months to November. ONS did, however, report a slowdown in the rate of growth in vacancies.

Omicron hits retail sector

While the latest official statistics revealed stronger than expected retail sales growth in November, more recent survey evidence shows concerns over the Omicron variant has hit activity on the High Street.

ONS data showed that total retail sales volumes rose by 1.4% in November, beating analysts’ expectations of a 0.8% rise. ONS Statistician Heather Bovill said sales were boosted by “strong Black Friday and pre-Christmas trading” adding that “clothing stores fared particularly well and exceeded their pre-pandemic level for the first time.”

The latest Distributive Trades Survey published by the Confederation of British Industry (CBI), however, suggests sales growth fell back sharply last month, with its headline net balance of retailers reporting sales growth slumping to +8 in December, down from +39 the previous month. This represents the lowest reading since non-essential shops were in lockdown last March.

Perhaps unsurprisingly, the survey also found that sales are expected to grow at a similarly lacklustre pace in January. Commenting on the data, CBI Principal Economist Ben Jones said, “Our December survey confirms what we’ve been hearing anecdotally about Omicron’s chilling impact on activity on the High Street, with retail sales growth slowing and expectations for the coming month sharply downgraded.”

It is important to take professional advice before making any decision relating to your personal finances. Information within this document is based on our current understanding and can be subject to change without notice and the accuracy and completeness of the information cannot be guaranteed. It does not provide individual tailored investment advice and is for guidance only. Some rules may vary in different parts of the UK. We cannot assume legal liability for any errors or omissions it might contain. Levels and bases of, and reliefs from, taxation are those currently applying or proposed and are subject to change; their value depends on the individual circumstances of the investor. No part of this document may be reproduced in any manner without prior permission.